Andrew L. Berkin, PhD

Jacob Pozharny, PhD

Recently the large cap US S&P 500 index hit an all-time high, closing above its previous high set two years ago in January 2022. Does this mean the S&P 500 is due for an imminent crash?

In the 1920s radio was the hot technology and the stock prices of associated companies soared. The poster child was the Radio Company of America (RCA), whose price rose from $43 a share in 1926 to a peak of $568 in September 19291, with a P/E ratio of 722. The stock market crash that commenced with Black Monday that month brought RCA’s stock price back to Earth, falling to $15 in 1932. It wasn’t until the 1960s that RCA regained its former high. A presumably apocryphal story is of an older man going to a brokerage to sell his long-held RCA shares, proclaiming, “Even money!” Needless to say, having an investment return of nothing for over three decades is not desirable.

Fast forward to the 1980s. Japanese technology, manufacturing, and real estate are on top of the world. On December 29, 1989, Japan’s benchmark Nikkei 225 hit an all-time high of 38,915.87, with a forward P/E ratio of over 503. Japan’s bubble economy subsequently burst, and the Nikkei fell sharply, dropping below 7,000. Fast forward again to recent times. On February 22, 2024, the Nikkei 225 closed at 39,098.68, finally breaking through its prior record high. After a span of over three decades, “Even money!”

Recently the large cap US S&P 500 index also hit an all-time high, closing above its previous high set two years ago in January 2022. Does this mean the S&P 500 is due for an imminent crash? The answer is no. The S&P 500 may fall or rise from here, but hitting an all-time high will not be the reason4. Since stocks tend to go up over time, all-time highs are common events. RCA and the US market hit many all-time highs before crashing in 1929; similarly with the Nikkei prior to its crash in 1989. In those cases, the rise in prices eventually far outstripped the rise in fundamentals, such as earnings, leading to extreme valuations. While the valuation of the S&P 500 today is elevated relative to history, it is below levels of a few years ago as well as in 1929 and 20005.

An important takeaway is that valuations do matter. Certainly, other factors such as quality and sentiment also drive returns, which is why we use them as well as value. Stocks can be cheap for a reason; they can also be expensive for a reason. And there were good reasons for the initial rise of both RCA and the Nikkei. RCA was a leader in both radio manufacturing and broadcasting, hot growth areas at the time. The Japanese economy boomed in the 1980s as exports soared. But as the Wall Street saying goes, “trees don’t grow to the sky”. At some point, stocks can get too expensive, and subsequently fall precipitously6.

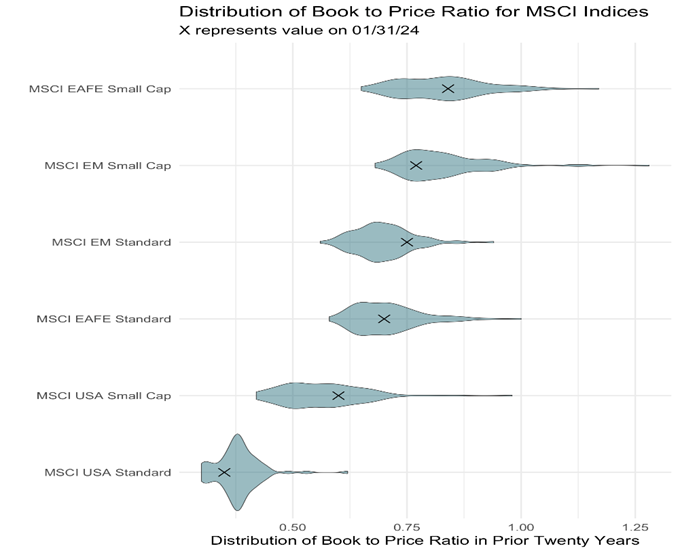

If valuations matter, where can one find attractive valuations today? One place is smaller cap stocks, whose returns have lagged their larger cap peers in recent years. Around the world, smaller cap stocks are priced more attractively relative to fundamental measures of value than their larger brethren. This holds true in the United States, other developed markets, and emerging markets. For example, the figure below shows that using Book to Price as a value measure, US small caps are cheaper than US large caps, EAFE (developed markets) small caps are cheaper than EAFE large caps, and EM small caps are cheaper than EM large caps. As noted, valuation is not the only driver, and there are other reasons why smaller cap stocks are attractive. We have discussed the case for smaller cap stocks in the United States7 and emerging markets8 in some recent pieces.

Source: FactSet, Bridgeway analysis

Value stocks do tend to have higher subsequent returns than their more expensive peers, a finding that goes back to at least Benjamin Graham9. For stock indices, Robert Shiller showed cheaper valuations tend to produce higher return over the next ten years (see footnote 5). Thus, valuations can be useful for setting long-run return expectations but have less short-term effect. Structural issues such as liquidity and legal protections also affect valuation levels. For example, the United States tends to have higher valuations than other markets. But if you believe in value investing, small caps are an interesting opportunity.

Note this is not a call to make a major tactical asset allocation shift. As always, diversification is important. And timing shifts in the market is nigh impossible. But for those whose allocation to small caps has moved away from target due to the run up in large cap stocks, rebalancing is well warranted. Given the discrepancy in valuations, investors may wish to revisit their return assumptions and consider an increased allocation to smaller stocks. And for those who have been ignoring smaller cap stocks in any of these markets, now is a good time to consider adding this asset class to your allocation.

- See for example “Bubbles and Crashes: The Boom and Bust of Technological Innovation” by Brent Goldfarb and David A. Kirsch. Prices are split adjusted. ↩︎

- See https://www.gold-eagle.com/article/rca-1925-1929-and-microsoft-1994-1998-0. ↩︎

- Data from Refinitiv; see https://finance.yahoo.com/news/nikkei-parties-1989-scales-record-033844899.html. ↩︎

- See also https://www.buckinghamstrategicwealth.com/resources/investing/all-time-market-highs. ↩︎

- See for example the Cyclically Adjusted PE (CAPE) ratio, http://www.econ.yale.edu/~shiller/data.htm. ↩︎

- Also see Party Like It’s 1972 for a discussion of the Nifty Fifty craze of the early 1970s. ↩︎

- https://bridgeway.com/perspectives/waiting-on-the-world-to-change-small-cap-value-investors/ ↩︎

- https://bridgeway.com/perspectives/why-emerging-markets-small-cap-2/ ↩︎

- For a thorough discussion of value, as well as other factors, see “Your Complete Guide to Factor-Based Investing: The Way Smart Money Invests Today” by Andrew L. Berkin and Larry E. Swedroe. ↩︎

DISCLAIMER AND DISCLOSURE

The opinions expressed here are exclusively those of Bridgeway Capital Management (“Bridgeway”). Information provided herein is educational in nature and for informational purposes only and should not be considered investment, legal, or tax advice.

Past performance is not indicative of future results.

Investing involves risk, including possible loss of principal. In addition, market turbulence and reduced liquidity in the markets may negatively affect many issuers, which could adversely affect client accounts.

Diversification neither assures a profit nor guarantees against loss in a declining market.

The Price-to-Earnings (P/E) Ratio is the ratio for valuing a company that measures its current share price relative to its earnings per share (EPS). The price-to-earnings ratio is also sometimes known as the price multiple or the earnings multiple.

The book-to-price ratio is a financial metric that compares a company’s current book value to its market value. It’s calculated by dividing the book value per share by the current stock price per share.

The Nikkei 225, also commonly referred to simply as the Nikkei or the Nikkei index, is the leading stock market index for Japan. It tracks the performance of 225 large, publicly traded companies listed on the Tokyo Stock Exchange (TSE).

The S&P 500 Index is a broad-based, unmanaged measurement of changes in stock market conditions based on the average of 500 widely held common stocks.

The MSCI EAFE Standard, also known as the MSCI EAFE Index, is an equity index that captures large- and mid-cap representation across 21 developed markets countries around the world, excluding the US and Canada. The MSCI EAFE Small Cap Index is an equity index that captures small cap representation across developed markets countries around the world, excluding the US and Canada.

The MSCI USA Standard, also known as the MSCI USA Index, is designed to measure the performance of the large- and mid-cap segments of the US market. The MSCI USA Small Cap Index is designed to measure the performance of the small-cap segment of the US equity market.

The MSCI EM Standard, also known as the MSCI Emerging Markets Index, captures large- and mid-cap representation across 24 emerging markets countries. The MSCI Emerging Markets (EM) Small Cap Value Index captures small-cap securities exhibiting overall value style characteristics across 24 emerging markets countries.

One cannot invest directly in an index. Index returns do not reflect fees, expenses, or trading costs associated with an actively managed portfolio.