Andrew L. Berkin, PhD

Christine Wang, CFA, CPA

In their 2020 book The Incredible Shrinking Alpha[1], Larry Swedroe and Andrew Berkin noted, “The financial equivalent of the quest for the Holy Grail is the quest for money managers who will deliver alpha, defined as returns above the appropriate risk-adjusted benchmark.” Alpha is typically measured as returns unexplained by conventional academic models using factors such as the market, size, value, momentum, profitability, and quality for equity portfolios[2]. The book provides the reasons and evidence for why alpha has been shrinking.

Many money managers work tirelessly seeking this elusive alpha. Yet, in this piece, we claim that there is, in fact, alpha to be found in a more straightforward manner. Does this contradict the Incredible Shrinking Alpha book? The answer is no. Rather than toiling over idiosyncratic name-by-name stock selection or trying to time the market, this incredible structural alpha can be found with thoughtful consideration of the factors driving returns and the portfolios designed from them.

This piece is a shorter version of a full paper with more details. We include two exhibits. Panel A of Exhibit 1 shows annualized returns of a 5×5 grid of all US stocks listed on major stock exchanges with positive book value, sorted on size and value as measured by book to market (B/M). High (low) B/M refers to the deepest (least) value stocks by this measure. A few features stand out. The smallest and deepest value stocks in the lower right have the highest returns at over 16% annually. In contrast, the smallest low value stocks in the lower left corner have the lowest returns. Generally, the deepest-value stocks in the right column have higher returns than the low-value stocks in the left column. The exception is for the largest quintile of stocks in the top row, where the returns are comparable. Value as measured by B/M has paid off over the long term, except for the largest stocks. Generally, smaller size has paid off too, and the smallest deepest value stocks have the highest returns.

Exhibit 1:

We’ve been looking at returns, but what about alpha or risk-adjusted returns? To measure alpha, we adjust using a Fama-French-Carhart four-factor model to see what returns are unexplained by the market, size, value, and momentum. Results are in Panel B. For the largest stocks, the low value stocks have positive alpha while high value has negative alpha, despite their comparable returns. The largest low (high) value stocks have exceeded (lagged) return expectations based on their B/M characteristics. Meanwhile, we find that the smallest and deepest value stocks indeed have strong and statistically significant alpha. These stocks have excess returns beyond what one might expect from their small and deep value characteristics; portfolios constructed with greater weight to this segment of the market would benefit from these higher-than-expected returns.

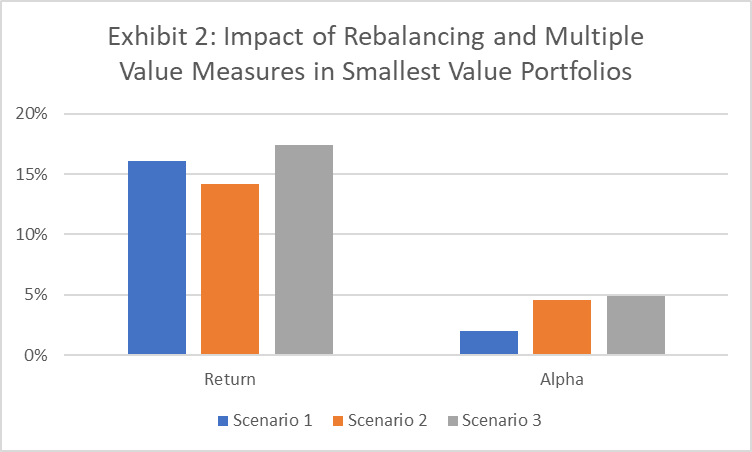

Delving deeper into the smallest and deepest value portfolio, Scenario 1 of Exhibit 2 (blue bars) represents the typical academic protocol used for factor models of rebalancing just once a year. But new data comes in constantly. Scenario 2 (the orange bars) shows what happens when we rebalance quarterly and use timely price information. Compared to Scenario 1, more timely data increases alpha by over 2.5% annually. These are extra returns not captured by the slower-moving academic factor models.

Exhibit 2:

But note that the raw returns decrease by almost 2%. Why? The reason is momentum. By rebalancing more frequently, we include more stocks that have recently dropped in price and thus have negative momentum. Now, alpha is nice, but at the end of the day, what investors can spend is the raw return. A way out of this problem is to screen the portfolio for these “falling knives” and avoid buying stocks that have seen large price drops. This helps remove the unwanted exposure to negative momentum.

Book to market is just one way to measure value, but there are others. Scenario 3 (grey bars) forms a “combo” value measure using B/M, sales to price, earnings to price, and cash flow to price as well as screens out the worst quintile of momentum names. This combo measure uses data from the balance sheet, top and bottom of the income statement, and the statement of cash flows. While returns from these measures are correlated, combining them provides diversification benefits. Returns and alpha both increase notably. Why does this extra return also manifest itself as alpha? It’s because the factor model is based just on B/M; this structural switching to multiple value metrics provides a boost not captured by B/M alone.

This momentum screen is one example of avoiding groups of stocks to provide structural alpha. In a similar manner, one can also avoid stocks with poor profitability. One can also avoid other “bad actors” such as penny stocks, recent IPOs, stocks with high costs to borrow, and stocks in bankruptcy.

Implementation matters tremendously as well. Poor implementation can hurt returns and alpha; disciplined implementation can be additive to both. This means trading patiently, providing liquidity to the market. Having a good number of stocks to choose from helps greatly, rather than needing to trade in a set of given names. Setting bounds on individual positions and sector weights aids in keeping a diversified portfolio while still targeting the desired factors. And securities lending brings in extra returns, especially in market segments like small value where a greater number of hard-to-borrow stocks are located.

Finally, one may wonder, if this is structural alpha, can one structure an index fund to access it? For existing index funds, the answer is an emphatic no! Most indexes don’t target the smallest deepest value stocks we highlight here, and many index providers use only B/M as their value measure and reconstitute their indexes less frequently. Furthermore, all index funds must buy the exact stocks at the exact weights on the exact dates, which doesn’t necessarily allow for the most efficient implementation. But managers actively targeting their desired exposures and actively managing their implementation can certainly attain this structural alpha.

While alpha from market timing and individual stock selection may be shrinking, one can still add value by targeting the factors that provide a premium. And as we have shown in this article, one can further add alpha above the returns explained by these factors. The sources of this alpha include deeper factor exposure, multiple metrics to evaluate a factor, timely rebalancing of portfolios, taking other factors such as momentum into consideration, avoiding bad actors, and disciplined implementation. These are some of the many details Bridgeway considers when constructing thoughtfully structured portfolios. We believe these details are worthwhile and we continue to pursue the research and discipline required to achieve this structural alpha.

For a PDF download of this piece, please use the following link:

The Incredible Structural Alpha

[1] See https://www.amazon.com/Incredible-Shrinking-Alpha-Escape-Clutches/dp/0692336516

[2] For more on factors, please reference Berkin and Swedroe’s Your Complete Guide to Factor-Based Investing.

DISCLAIMER AND DISCLOSURE

The opinions expressed here are exclusively those of Bridgeway Capital Management (“Bridgeway”). Information provided herein is educational in nature and for informational purposes only and should not be considered investment, legal, or tax advice.

Past performance is not indicative of future results.

Investing involves risk, including possible loss of principal. In addition, market turbulence and reduced liquidity in the markets may negatively affect many issuers, which could adversely affect client accounts.

Diversification neither assures a profit nor guarantees against loss in a declining market.

The book to market ratio compares a company’s book value to its market value. The book value is the value of assets minus the value of the liabilities. The market value of a company is the market price of one of its shares multiplied by the number of shares outstanding.

The sales to price ratio is a valuation ratio that compares a company’s revenue to its stock price It is an indicator of the value that financial markets have placed on each dollar of a company’s sales or revenues.

The earnings to price ratio is the ratio for valuing a company that measures its earnings per share (EPS) relative to its current share price. The earnings-to-price ratio is also sometimes known as the price multiple or the earnings multiple.

The cash flow to price ratio is a stock valuation indicator or multiple that measures a company’s operating cash flow per share relative to its stock price. The ratio uses operating cash flow (OCF), which adds back non-cash expenses such as depreciation and amortization to net income.