Andrew L. Berkin, PhD

Cindy Griffin, CIPM

Following up on our analysis of factor performance in rising interest rates1, recessions2, and bear markets3, we discuss the benefits of remaining invested in stocks and maintaining multi-factor diversification to help weather periods of high inflation.

After years of laying low, inflation emerged in 2021 and has remained elevated. In the United States, the annual rate of inflation as measured by the Consumer Price Index (CPI) was 3.7% as of September 2023. That’s down from its peak of 9.1% in June of last year, but still well above the rates we typically saw during the previous 10 years, when inflation rarely edged much higher than 2%.

We haven’t seen inflation numbers like these since the early 1980s, before the experience of many of today’s investors. The Federal Reserve has been raising interest rates in response. Both the S&P 500 and U.S. Treasuries fell in 2022 as yields rose; while the stock market has recovered this year, bond prices have continued their fall.

The situation is similar around the world, with inflation spiking and markets having fallen. There are a multitude of potential reasons for inflation’s unwelcome return, including ongoing supply chain issues that have made goods scarce, stimulus money that gave consumers more dollars to go after fewer goods, pent-up spending demand unleashed after the pandemic, a decades-long low-interest rate environment and deficit spending. But investors may be less concerned about the causes of inflation than they are about its impact on their portfolios.

Does high inflation always cause markets to drop? We don’t have to look very far back for a counterexample. Inflation was 7.0% in 2021 yet the S&P 500 soared by 28.71%. Contrary to screaming headlines, stocks can do quite well — as well as poorly — during high inflationary periods. That raises important questions about the actual relationship between inflation and stock performance.

In this piece, we examine how stocks have performed historically in different inflationary environments and compare them to the asset classes of bonds and cash. We start by giving brief conceptual arguments before examining historical data going back over a century. We next look at how different segments of the market, such as factors and sectors, have performed. To get even more data and show the robustness of our results, we then extend our work to over 20 developed markets. Finally, we close with some takeaways to guide investors looking ahead.

The highlights: Higher inflation isn’t always bad news for stocks, and it can affect the performance of different factors quite differently. And even when high inflation dampens equity returns, stocks still produce positive returns on average during high inflationary periods—and strongly outperform cash.

These results suggest that investors who let fears of high inflation drive them out of the stock market could be making a costly mistake.

How Might We Expect Markets to React to Inflation?

Reasons why inflation is bad for the stock market often involve that the central banks, such as the U.S. Federal Reserve, will raise interest rates to slow the economy and fight inflation. This slowing of the economy then leads to lower stock prices. Rising interest rates also bring higher discount rates, leading to lower stock valuations. But as we showed (see footnote 1), while higher rates do bring lower bond returns due to the bond math, there is no distinct relation with stock returns. Interest rates will rise because of a strong economy, which should bring higher earnings and cash flows.

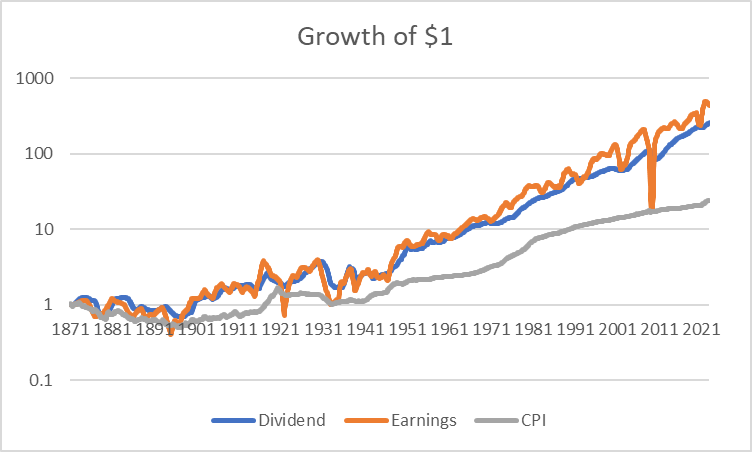

This argument is behind why some argue that stocks should provide a good inflation hedge. As prices in general go up, so should the sales, earnings, cash flows, and dividends of the companies in the stock market. Provided valuations such as P/E ratios stay the same, stocks should be a good match for inflation. We can see this in Exhibit 1, which uses over 150 years of US data from Robert Shiller’s website4. The plot shows the growth in earnings, dividends, and inflation from 1871 through 2022. Visually we get a long-term perspective. Earnings and dividend growth indeed track inflation over time, but at a higher level. This makes sense. Stocks allow the investor to participate in the growth of the economy, and that nominal growth has typically been higher than inflation. Recall that the most common measure of economic growth, gross domestic product or GDP, is typically given in real terms, meaning after inflation.

Exhibit 1: Growth of $1 in CPI, Dividends, and Earnings, 1871 – 2022

Source: Robert Shiller, Bridgeway calculations

Exhibit 2 puts numbers to the visual and moves to a yearly time frame by giving the correlation of inflation, earnings, dividends, and stock returns for the US. Inflation correlates at 27% and 20% with annual changes in dividends and earnings, respectively. This is modestly positive, but recall that earnings are smoothed by accounting items such as depreciation, amortization, and accounts receivable and payable. Dividends are discretionary, and companies smooth them in order to avoid dividend cuts, which are viewed poorly by the market. Such smoothing can reduce the correlation of earnings and dividends with inflation. Stock returns are even more modestly correlated with inflation at 13%. This is still positive, so stocks do provide a modest hedge to inflation at an annual level. But there is more going on, as the market is forward-looking and moves to perceptions of future cash flows and discount rates. With that said, let’s next look at how asset classes respond to inflation.

Exhibit 2: Correlations of Annual Changes in CPI, Dividends, Earnings and Stock Returns, 1871 – 2022

| CPI | Dividends | Earnings | Returns | |

| CPI | 1 | 0.27 | 0.20 | 0.13 |

| Dividends | 0.27 | 1 | 0.19 | 0.06 |

| Earnings | 0.20 | 0.19 | 1 | 0.29 |

| Returns | 0.13 | 0.06 | 0.29 | 1 |

Source: Robert Shiller, Bridgeway calculations

Stocks and Inflation in the U.S.

We start by examining how the United States stock market fares compared to the risk-free rate in different inflationary regimes. Inflation data is released monthly with a lag and is often subsequently revised. We avoid shorter-term timing and focus on annual returns. Such longer time frames lessen the impact of noise from short-term fluctuations, the details of timing, and transaction costs. Return data comes from the Ken French data library5, while inflation comes from the Federal Reserve6. We go from the start of annual returns in 1927 through 2022, giving us a 96-year history.

Exhibit 3 shows the returns of US stocks and the risk-free rate (cash, as given by one-month T-bills) according to the same year’s level of inflation. While we explain how to interpret these exhibits, readers whose eyes glaze over at tables of numbers can ignore them and simply focus on the explanation in the paragraphs below.

There are three sets of five columns. The three sets give the amount of inflation, stock market returns, and risk-free returns. The five columns represent different quintiles of inflation; the 19 years of lowest inflation are on the left, while the 20 years of highest inflation are on the right. By definition, average inflation increases from -1.52% in the lowest inflation quintile to 8.63% in the highest quintile. From the “Min” row, inflation of 4.86% or higher puts a year in the highest quintile. The 7.04% and 6.45% inflation of 2021 and 2022 are solidly into the highest quintile of inflation, for example, although well below the all-time high of 18.13% (reached in 1946 as prices spiked in the aftermath of World War II). The next five columns show stock returns grouped according to inflation quintiles, while the last five columns show cash as given by the risk-free rate, also grouped according to inflation quintiles.

Exhibit 3: Stock and Risk-free Returns Dependent on Same Year Inflation (all in %) 1927-2022

Source: Ken French data library, Federal Reserve FRED data library, Bridgeway calculations

We can see that stock returns are consistently positive in each of the five inflationary regimes. However, there is great fluctuation, as seen by the high standard deviations and the spread of the minimum and maximum returns. Returns are highest and quite statistically significant for the middle three inflationary quintiles. Stocks are not as strong on average when inflation is low or negative. This aligns with our argument that stocks might follow prices; when sales and earnings are kept low by deflation, there is little growth to reflect in stocks.

When inflation is highest, stock returns are still nicely positive at 5.84% annually. High inflation does not necessarily mean that stocks will fall; indeed, on average they do just fine. But our caveat of great fluctuations still applies here; in any given year results could be much better or much worse.

Also, note that the average return is not just nicely positive, it is also higher than the average short-term interest rate of 5.03%. Investors who panic about their stock holdings and move into cash when inflation is high tend to do worse. In fact, the term “risk-free” rate is a misnomer from a real inflation-adjusted perspective. When inflation is high, holding cash doesn’t keep up with rising prices, and investors lose purchasing power. On average, stocks also lag inflation when the latter is high, but they do outperform cash.

One could wonder, if I see high inflation now, what will happen in the future? We address this in Exhibit 4. The first five columns tell us the level of inflation based on the inflation of the prior year. We still see that the averages move from low to high as we go from quintile 1 to quintile 5. Inflation is sticky; high or low inflation in one year tends to be repeated the next year. But it is not guaranteed. For example, the highest annual inflation of 18.13% in 1946 is now in the middle quintile, as it followed the moderate 2.25% inflation of 1945.

What is of particular interest to the investor is what happens to stocks and cash. After a year of high inflation, stocks now do quite well, with an average return of 11.07%. This is on par with the returns of the other quintiles, as well as the long-term average of 11.84% for this period. There is plenty of variation from year to year, as can be seen from the standard deviation as well as minimum and maximum, but this is always true for stocks. Cash yields remain elevated in years following high inflation, as the Fed keeps rates elevated. But now, those cash returns are trounced on average by the return of stocks. The upshot for investors? If you pull out of stocks because inflation is high, not only do you get worse returns on average in the current year, but you also risk missing out on the subsequent strong performance of stocks in the following year.

Exhibit 4: Stock and Risk-free Returns Dependent on Prior Year Inflation (all in %) 1927-2022

Source: Ken French data library, Federal Reserve FRED data library, Bridgeway calculations

Inflation and Segments of the Market

While those results make a case that the stock market as a whole delivers positive returns across inflationary regions, what about different segments of the market? Perhaps some do better than others in periods of high inflation?

We first examine the performance of factors — groups of stocks defined by certain characteristics. For example, a common academic version of the value factor, HML, is given by the return of the highest 30% of stocks by book-to-market (B/M) minus the lowest 30%. We use common definitions from the Ken French data library. We show only the average returns by inflationary regime to save space, but suffice it to say that again there is plenty of variation around those averages.

Exhibit 5: Average Factor Returns (%) Dependent on Same Year Inflation

(1927-2022 for Mkt-Rf, SMB, HML, and UMD)

(1964-2022 for RMW and CMA)

| Infl Lo20 | Infl Q2 | Infl Q3 | Infl Q4 | Infl Hi20 | |

| Mkt – Rf | 7.47 | 14.29 | 12.20 | 8.39 | 0.81 |

| SMB | 0.83 | 5.23 | 4.84 | 3.20 | 0.60 |

| HML | 0.23 | 2.68 | 4.16 | 5.58 | 9.26 |

| UMD | 11.65 | 8.35 | 4.98 | 10.87 | 9.49 |

| RMW | 5.69 | -0.34 | 2.91 | 6.31 | 3.39 |

| CMA | -2.00 | 4.52 | 2.72 | 2.59 | 6.75 |

Source: Ken French data library, Federal Reserve FRED data library, Bridgeway calculations

The first row (Mkt-Rf) is simply the equity risk premium — the market’s return relative to the risk-free rate. It is the same as subtracting the appropriate two columns in Exhibit 37, and highlights that excess stock returns are lowest when inflation is high, but still positive.

The remaining rows show how different factors perform in different inflationary environments (again grouped by quintile). For example, smaller stocks always show a premium, but it is lower when inflation is either very high or low. Most other factors8 demonstrate no clear pattern, with one notable exception: Value.

As inflation increases, the value premium (as represented by HML) increases as well in a monotonic fashion. This is in exact agreement with what we showed by looking at decades from our perspective Does Value Just Need Some Growth?9 While there is plenty of variation (not shown to save space), on average, value performs best when inflation is higher.

We look at returns by sector in Exhibit 6. Generally, returns are lowest in the low and high inflation quintiles, in keeping with the overall pattern of the market returns we saw in Exhibit 3. Otherwise, there is again little noticeable pattern, with the exception of Energy. For this sector, returns rise monotonically with inflation, climbing from 4.89% on average in the low inflation quintile to 21.42% when inflation is high. This perhaps reflects the special role of energy in powering the economy and helping to drive consumer prices. Certainly, the Energy Crisis of the 1970s drives some of this behavior, but we see a similar pattern in other periods of high inflation, as well as currently.

Exhibit 6: Average Sector Returns (%) Dependent on Same Year Inflation (1927-2022)

| Infl Lo20 | Infl Q2 | Infl Q3 | Infl Q4 | Infl Hi20 | |

| Nondurables | 9.04 | 15.67 | 11.81 | 20.26 | 5.06 |

| Durables | 20.04 | 30.02 | 15.20 | 10.10 | 4.46 |

| Manufacturing | 10.52 | 16.90 | 17.27 | 15.23 | 5.78 |

| Energy | 4.89 | 8.99 | 11.63 | 18.10 | 21.42 |

| Chemicals | 15.61 | 14.45 | 12.13 | 14.97 | 5.93 |

| Business Equipment | 11.96 | 20.17 | 23.60 | 12.31 | 4.60 |

| Telecom | 6.83 | 17.29 | 16.44 | 10.40 | 2.50 |

| Utilities | 7.91 | 10.58 | 15.82 | 15.94 | 5.62 |

| Shops | 11.46 | 22.09 | 11.18 | 18.81 | 3.33 |

| Health | 10.08 | 21.06 | 11.19 | 18.19 | 7.42 |

| Finance | 8.36 | 14.85 | 15.47 | 19.71 | 5.85 |

| Other | 5.86 | 17.88 | 10.64 | 13.36 | 5.07 |

Source: Ken French data library, Federal Reserve FRED data library, Bridgeway calculations

Developed Markets: How Do Stocks, Bonds, and Cash Respond to Inflation?

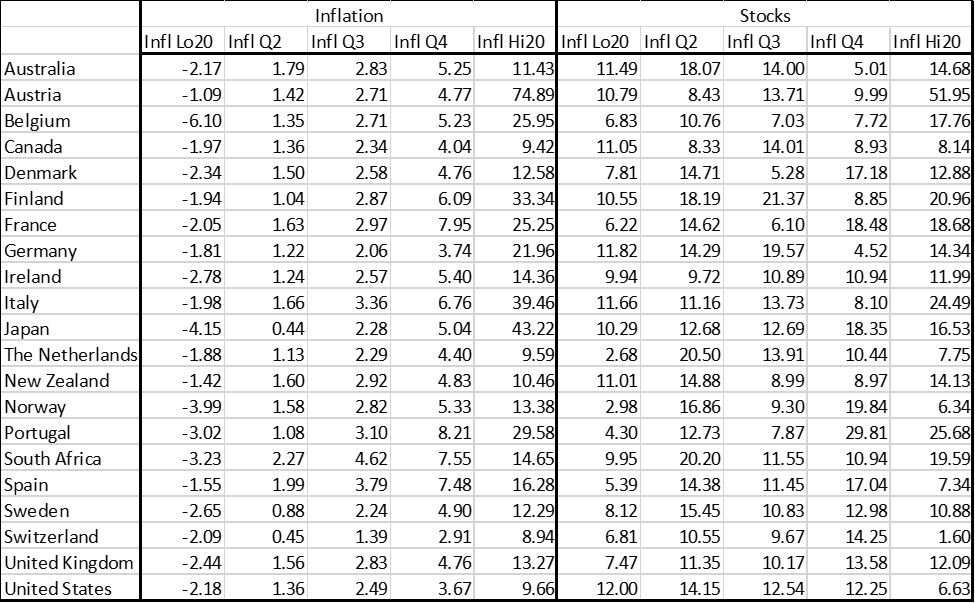

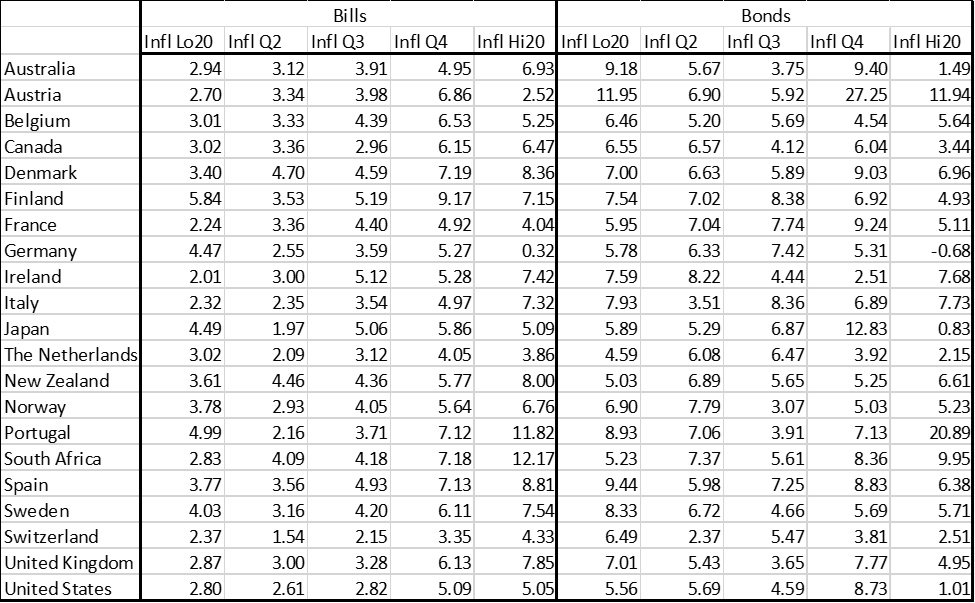

Until the recent spike, inflation had been quiescent in developed markets since the early 1980s. To get a full sampling of inflationary regimes, we therefore require a long history. For examining inflation and the returns of the major asset classes of stocks, bills, and bonds, we utilize data for 21 developed markets going back to 1900 from Dimson, Marsh, and Staunton (DMS)10, augmented by Bloomberg and the OECD11 in recent years. We are interested in inflation and returns from the perspective of a local investor and so use local nominal returns. We omit the hyperinflation years of 1922 and 1923 for Germany and 1922 for Austria so as not to excessively skew results; suffice it to say that when inflation is over 1000% annually, investors are miserable as returns in any asset class fail to keep pace.

Results are given in Exhibit 7. Panel A shows inflation and stock returns, Panel B shows bill and bond returns. Let’s focus on the United States first since it is easily viewable at the bottom of both panels, and we’ve looked at similar data in Exhibit 3, although from another source and a somewhat shorter history. Just as we saw earlier, when inflation is highest then stock returns are lowest, although still nicely positive. Also, as before, this is the only one of the five inflationary regimes where stocks do not keep up with inflation, gaining 6.63% on average while inflation is at 9.66%. But also as before, stocks still provide a risk premium relative to cash even when inflation is high (and indeed in all regimes). What is new here is that we also have bond returns, and these are lowest when inflation is high at 1.01% annually. This makes intuitive sense, as investors will demand a higher yield with higher inflation, causing bond prices to fall. Thus, while stock returns will vary, when inflation is high on average their return is better than both cash and bonds. This is a key insight for investors: if you sell out of stocks because of inflationary fears, on average you would have done worse parking your money in either cash or especially bonds.

Examining all 21 countries shows a similar pattern. In 17 out of 21 countries, stocks fail to beat inflation when the latter is high. Most of the four countries where stock returns are higher are known for having a large amount of their economy dependent on commodities, which as we saw with energy can rise with or cause inflation. But in none of the countries do cash or bond returns keep pace with high inflation. And in almost all countries, stocks are the best asset class when inflation is high. The only exceptions are Norway and Spain where bills are best in high inflation, and Switzerland where both bills and bonds beat stocks in high inflation regimes. But looking at the full set of 21 developed markets over 123 years, stocks are clearly the highest returning asset class on average when inflation rears its head.

Exhibit 7: Stock, Cash, and Bond Returns (%) Dependent on Same Year Inflation in Local Currency

Panel A

Panel B

Source: DMS, Bloomberg, OECD, Bridgeway calculations

Key Takeaways

The market’s poor performance in 2022 has many investors worried that high inflation automatically means bad news for stocks. However, history shows that has not always been the case. For US markets, and international developed markets as well, high inflation environments have still produced positive absolute returns in the stock market on average. These results suggest that allowing fears of an inflationary environment to drive investment decisions out of stocks and into cash or bonds could be a very costly mistake.

The performance of factors, however, is not equal across inflationary environments. Investors should be aware that some factors may perform better or worse in different inflation environments. In the US, for example, value appears to perform better than average in higher inflation environments, while smaller cap stocks tend to perform better when inflation is low. While we don’t recommend timing factor performance, the historical evidence of these factors’ performance could be a preview of what’s to come.

As always, investors should approach these results with some caution. While the average return of stocks in high inflation environments is positive, the variation of returns from year to year can be large. An investor’s experience in one year can be very different in another. Further, we have fewer observations in our evidence on factor performance, and those observations tend to be in lower inflation environments, which may obscure a full picture of factor performance in high inflation environments.

For many investors today, inflation is a new experience. But inflationary fears shouldn’t be the driving force behind whether to get out of stocks. In fact, the opposite may be true given the historical evidence that around the world, stocks have outperformed both bonds and cash in periods of high inflation. And as always, exposure to the factors that drive equity returns can provide additional benefits.

- Berkin, Andrew L. 2018. “What Happens to Stocks when Interest Rates Rise?” Journal of Investing 27 (2): 126-135. ↩︎

- https://bridgeway.com/perspectives/stress-test-how-factors-perform-before-during-and-after-recessions/ ↩︎

- https://bridgeway.com/perspectives/factoring-in-bear-markets/ ↩︎

- https://www.econ.yale.edu/~shiller/data.htm ↩︎

- https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html ↩︎

- https://fred.stlouisfed.org/ ↩︎

- For example, when inflation is in the highest quintile, Exhibit 3 shows stock market and risk-free rate returns of 5.84% and 5.03% on average, and 5.84% – 5.03% gives the 0.81% return seen here. ↩︎

- Other factors represented in Exhibit 5 are momentum as represented by Up-Minus-Down or UMD, profitability as represented by Robust-Minus-Weak or RMW, and investment as represented by Conservative-Minus-Aggressive or CMA. ↩︎

- https://bridgeway.com/perspectives/does-value-just-need-some-growth/ ↩︎

- https://www.tinyurl.com/DMSdata ↩︎

- https://data.oecd.org/ ↩︎

DISCLAIMER AND DISCLOSURE

The opinions expressed here are exclusively those of Bridgeway Capital Management (“Bridgeway”). Information provided herein is educational in nature and for informational purposes only and should not be considered investment, legal, or tax advice.

Past performance is not indicative of future results.

Investing involves risk, including possible loss of principal. In addition, market turbulence and reduced liquidity in the markets may negatively affect many issuers, which could adversely affect client accounts.

Diversification neither assures a profit nor guarantees against loss in a declining market.

The Consumer Price Index (CPI) is a measure of how much the prices of consumer goods and services have changed over time.

The S&P 500 Index is a broad-based, unmanaged measurement of changes in stock market conditions based on the average of 500 widely held common stocks. One cannot invest directly in an index. Index returns do not reflect fees, expenses, or trading costs associated with an actively managed portfolio.

The price-to-earnings ratio (P/E) is a way to value a company by comparing the price of a stock to its earnings. It is calculated by dividing the current price of a common share by the earnings per common share.

Gross domestic product (GDP) is the total monetary value of all goods and services produced within a country’s borders during a specific time period. GDP is used to evaluate a country’s economic health.

High Minus Low (HML) is a value premium; it represents the spread in returns between companies with a high book-to-market value ratio and companies with a low book-to-market value ratio.

The book-to-market ratio compares a company’s book value to its market value. The book value is the value of assets minus the value of the liabilities. The market value of a company is the market price of one of its shares multiplied by the number of shares outstanding.